Black-Scholes: A Quantum Perspective

An investigation into how the Black-Scholes equation is actually embedded in the dynamics of quantum particles.

Recently, I started learning stochastic calculus and stumbled upon the famous Black-Scholes (BS) equation which gives a model to price an option (a financial derivative where the buyer has the option to buy or sell a security at a pre-determined price at a later date). The core of this pricing theory is coming up with the risk neutral measure, where you replicate the payoff of the option using a portfolio of stocks and cash. So, when you calculate the time valued price of the portfolio at the current time, you will obtain the theoretical price of the option.

This is all fun, but I was wondering if you can look at the BS model from a different light. Being a physics enthusiast, I looked for an area of physics that also dealt with uncertainty and probability. So, what better area than Quantum Mechanics. I tried to look at the BS model as an instance of the famous Schrodinger’s equation. I am going to assume you have some familiarity with quantum mechanics, but if you are not familiar with QM, just give the wikipedia page a quick read for the basics and you should be able to follow this article.

Schrodinger Equation

Everyone has heard of Schrodinger’s cat, the poor creature that is dead and alive from the radiation (or poison depending on whom you ask). It is an example of superposition of states, but we will not concern ourselves with that now. The lesser known (to the general public of course), but much more exciting equation is the Schrodinger equation. It is similar to Newton’s laws, but applied to particles. Actually, Schrodinger equations are the QM analog to Hamiltonian mechanics in classical mechanics, as both use the Hamiltonian operator to develop a differential equation that describes the motion (or wavefunction) of a particle.

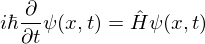

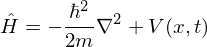

We only concern ourselves with the time dependent Schrodinger equation, which can be written as the following:

Where,

If we are dealing with position space. In more general terms, the equation is

Now that we know what the Schrodinger equation is, we can take a look at the BS equation.

Black-Scholes Equation

Without going into much of the derivation, the BS equation is a PDE that relates the option price, usually denotes as C, to factors such as price of security, S, time of expiry, T, volatility, risk free interest, r, and current time, t. So, the equation is as follows:

One thing to note is that according to the BS equation, the stock price at time T follows the following distribution:

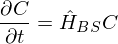

This will be important is verifying that the QM perspective is in fact accurate. Now, we can go on to develop a Schrodinger BS equation that would give us the option price.

Quantum BS Equation

Now, by just inspecting the two equations above, we can see some similarity, and suggests the following form for the Quantum Mechanical Black-Scholes (QMBS) equation:

By making the following transformation,

We can write the Hamiltonian as

Note that this Hamiltonian is not a Hermitian operator, so most of the elegant simplifications in QM might not apply. However, we can still proceed to see how this equation may be tackled.

Now we define a probability, p(x, y, T-t; x’, y’) as the probability that the price x and volatility y at time t, will become price x’ and volatility y’ at time T. Letting T-t to be tau, g(x,y) to be the payoff of the option, and noting the following

We get the following solution for the option price

Those of you who have done some work on PDE or have some knowledge of QM would recognize that

is actually a kernel (Green’s function) for the QMBS equation.

Solving QMBS Equation

Now we try to tackle the QMBS equation. From

We get the following solution for the option price

It is useful now to switch to Dirac notation:

So, we now get

Now, we can write the full solution in terms of the payoff function

This can be written in a different way by using the completeness relation

Comparing with our kernel form of the solution, we deduce that

This in fact reminds us an awful lot of the risk neutral pricing and time value of money. To find an explicit solution, we are going to analyse the equation in momentum space in of position space. So, in momentum space, our BS hamiltonian becomes

Also,

Using the standard momentum position relations, we get

Where

Now we can evaluate the explicit solution

Evaluating this Gaussian integral (with some massaging), we obtain the following solution for the probability distribution

This has the same distribution for the stock price at time T as the BS model

Now that means that both approaches are valid as they result in the same solution.

Conclusion

It is indeed very interesting to investigate the connections between branches of mathematics and physics. Who would’ve thought that the Black-Scholes equation, which is used to value options in finance, would be an instance of Schrodinger equation, used to describe the wavefunctions of particles. It is in such moments that the beauty of mathematics is revealed, and in some sense, that phenomenon across disciplines can always be described with the same mathematical equations and postulates.